The supervision of the banks in the Eurozone.

A key pillar of the so called ‘banking union’ was the establishment of the Single Supervisory Mechanism (SSM). The SSM introduced a new structure for the prudential supervision of banks and banking groups in the Eurozone[2] . The SSM involves close cooperation between the ECB and the national competent/supervisory authorities (NCAs) in participating member states.

Since 4 November 2014, “significant”[3] banks in participating countries have been under the direct supervision of the European Central Bank[4]. Smaller banks[5] continue to be directly monitored by the relevant NCA, although the ECB has the authority to take over direct supervision of any bank. The SSM only deals with bank supervision. Supervision of the rest of the financial sector in the Eurozone (for example insurance firms) remains a national competence. In addition, some aspects of bank supervision (for example consumer protection) remain a task for national supervisors. All banks in member states participating in the SSM are subject to the Single Resolution Mechanism (SRM).

You can read more about

- the SSM here;

- the SRM here; and

- the banking union here

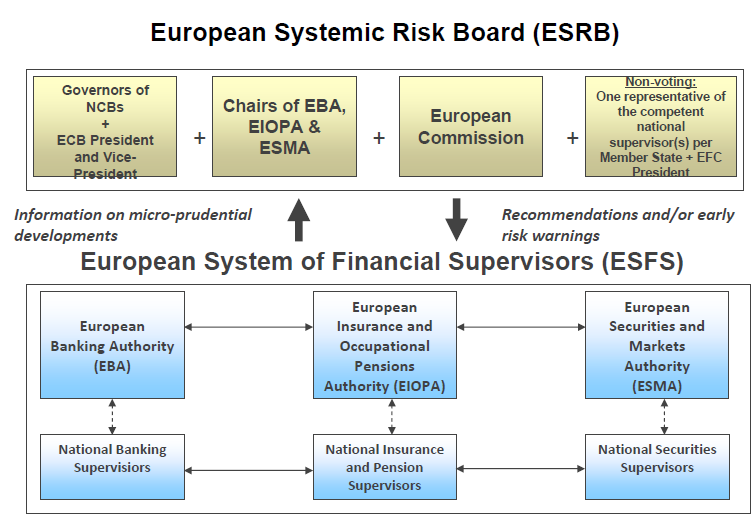

The broader system for financial supervision outside the SSM.

The supervision of individual firms (i.e. micro-prudential and conduct supervision) is dealt with by the NCAs (see further below). It is the NCAs that are in direct contact with firms.

At the European level, the ESFS is operated by

- the European Systemic Risk Board (ESRB) and

- the three European Supervisory Authorities (ESAs) for the financial services sector

- the European Banking Authority (EBA) based in London;

- the European Insurance and Occupational Pensions Authority (EIOPA) in Frankfurt; and

- the European Securities and Markets Authority (ESMA) in Paris.

Figure 1: Overview of the ESFS (source: European Commission)

The European Systemic Risk Board

The ESRB monitors and assesses potential threats to financial stability that arise from macro-economic developments and from developments within the financial system as a whole ("macro-prudential supervision"). Thus, the ESRB provides an early warning of system-wide risks that may be building up and issue recommendations for action to deal with these risks.

The ESRB monitors and assesses potential threats to financial stability that arise from macro-economic developments and from developments within the financial system as a whole ("macro-prudential supervision"). Thus, the ESRB provides an early warning of system-wide risks that may be building up and issue recommendations for action to deal with these risks.

The European Supervisory Authorities - organisation

Each ESA[6] has a Board of Supervisors, a Management Board and an Executive Director. The Board of Supervisors is composed of ‒

- the ESA (non-voting) Chairperson,

- the (voting) heads of the NCAs in each of the 28 Member States, and

- (non-voting) observers from the European Commission, the ECB, the ESRB, the other ESAs and the relevant NCAs.

The Executive Director participates in meetings of the Board of Supervisors.

A number of NCAs are represented on more than one ESA, reflecting the integrated nature of their national supervisory authority. Furthermore, some individuals sit on more than one Board of Supervisors.

Figure 2: Representation of the national competent authorities (NCAs) in the ESA’s Board of Supervisors. (Source: European Parliament/Mazars).

The Joint Committee of the European Supervisory Authorities has a coordination role on cross-sectoral issues such as the supervision of financial conglomerates. The structure of the sub-committee dealing with this area, for example, is shown below (see figure 2).

Figure 3: The joint committee structure. (Source: European Commission)

The European Supervisory Authorities – their role

The ESAs have various roles, mainly concerned with developing the EU rulebook and ‘system management’ for micro-prudential supervision. Supervision of individual firms, on a day to day basis, is still largely the responsibility of the relevant NCA/NSAs. The ESAs

The ESAs have various roles, mainly concerned with developing the EU rulebook and ‘system management’ for micro-prudential supervision. Supervision of individual firms, on a day to day basis, is still largely the responsibility of the relevant NCA/NSAs. The ESAs

- have a more direct supervisory role for only a few pan-European institutions (see below) ;

- coordinate cross-border supervision of groups by multiple NCAs, including colleges of supervisors;

- generally promote supervisory co-operation and co-ordination across Member States;

- conduct EU-wide risk assessments and stress testing;

- analyse the economics of financial markets to understand market structure and market failures;

- have emergency powers enabling the ESAs to demand national competent authorities take specific remedial actions, including temporary restrictions on financial products or activities;

- work to raise standards of supervision across Member States by issuing guidelines and instructions to NCAs (see further below);

- work to establish a single rulebook and a single supervisory handbook across the EU (see further below); and

- are involved in international discussions with regulators outside the EU.

The “Single Rulebook" and technical standards

The Single Rulebook concept is intended to provide a single set of harmonized prudential rules which institutions throughout the EU must respect, with uniform application of EU legislation in all Member States.

The ESAs contribute to this process by advising the European Commission (and other EU bodies) for example on delegated acts and itself developing binding technical standards (BTS). The ESAs also coordinate a Single Rulebook Q&A process for answering questions on the practical implementation of the legislation/rulebook. They also review the application of all BTS adopted by the European Commission and proposes amendments, if necessary.

The Single Rulebook concept is intended to provide a single set of harmonized prudential rules which institutions throughout the EU must respect, with uniform application of EU legislation in all Member States. The ESAs contribute to this process by advising the European Commission (and other EU bodies) for example on delegated acts and itself developing binding technical standards (BTS). The ESAs also coordinate a for answering questions on the practical implementation of the legislation/rulebook. They also review the application of all BTS adopted by the European Commission and proposes amendments, if necessary.

The European authorities can overrule national authorities

The ESAs are able to address decisions directly to national authorities in three areas:

The ESAs are able to address decisions directly to national authorities in three areas:

- In cases where they are arbitrating between national authorities involved in the supervision of a cross-border group and where they need to agree or coordinate their position;

- In cases where a national authority is incorrectly applying EU Regulations; and

- In emergency situations declared by the Council. Some situations, can, in theory, lead to the ESA eventually directing a decision to individual firms.

Direct supervisory powers

The European Securities and Markets Authority (ESMA) is also entrusted with exclusive supervisory powers over credit rating agencies registered in the EU (and will have a similar role in relation to trade repositories). It has investigatory, inspection and information powers.

The Authorities can ban toxic or high-risk financial products

The ESAs have powers to prohibit or restrict certain financial activities that threaten the orderly functioning and integrity of financial markets or the stability of the whole or part of the financial system in Europe. This applies where specified in sectoral legislation (such as, in the case of ESMA, the Regulation on short selling, MiFID II and PRIIPS) and also in the case of an emergency situation (as above).

[1] House of Lords European Union Committee 5th Report of Session 2014-15

Review of the European System of Financial Supervision (ESFS) (2013-14)

Review of the New ESFS by the Directorate-General for Internal Policies Policy Department

[2] EU member states outside the Eurozone can also join the SSM but none have done so to date.

[3] A bank is considered "significant" based on 5 conditions. The value of its assets exceeds € 30 billion. The value of its assets exceeds both € 5 billion and 20% of the Gross Domestic Product of the member state in which it is located. The bank is among the three most significant banks of the country in which it is located. The bank has large cross-border activities. The bank receives, or has applied for, assistance from Eurozone bailout funds. (In each participating country, at least the three most significant credit institutions are subject to direct supervision by the ECB, irrespective of their absolute size).

[4] Around 120 banking groups are supervised, representing approximately 80% of bank assets.

[5] Around 6,000

[6] Regulation No1093/2010 establishing a European Supervisory Authority (European Banking Authority), amending Decision No 716/2009/EC and repealing Commission Decision 2009/78/EC.

Regulation No 1094/2010 establishing a European Supervisory Authority (European Insurance and Occupational Pensions Authority), amending Decision No 716/2009/EC and repealing Commission Decision 2009/79/EC

Regulation No 1095/2010 establishing a European Supervisory Authority (European Securities and Markets Authority), amending Decision No 716/2009/EC and repealing Commission Decision 2009/77/EC

Social Media cookies collect information about you sharing information from our website via social media tools, or analytics to understand your browsing between social media tools or our Social Media campaigns and our own websites. We do this to optimise the mix of channels to provide you with our content. Details concerning the tools in use are in our privacy policy.